The growth of fintechs and payment institutions has brought new ways to structure financial operations in Brazil. Among these models, the so-called omnibus account has gained relevance for allowing greater agility and simplification in resource management.

At the same time, this model has begun to raise important discussions about transparency, traceability, and regulatory compliance.

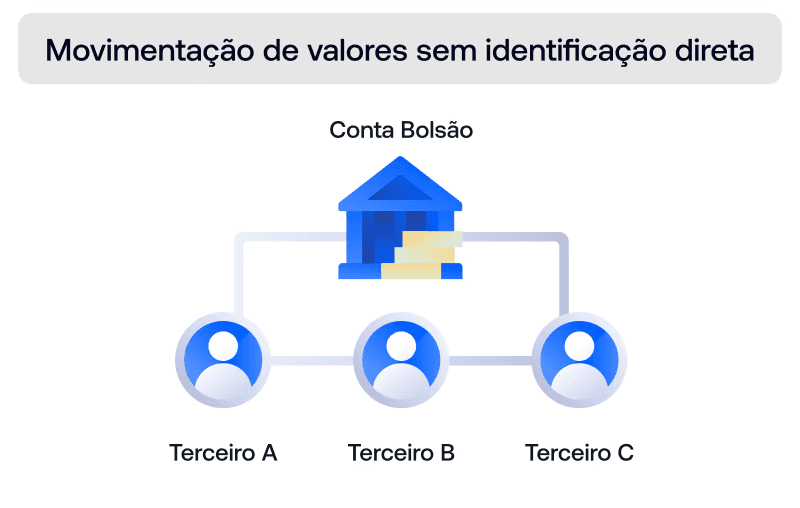

An omnibus account is a model in which the funds of multiple clients are held in a single bank account, usually in the name of the fintech or payment institution, without direct individualization in the financial system.

More than a technical concept, understanding how this model works—and what its risks are—is essential for companies that operate or intend to operate financial services.

What is a pooled account?

A pooled account is a structure in which a financial or payment institution holds the funds of multiple users in a single centralized account.

In practice:

The money from several customers is concentrated in a single account

The formal ownership of that account belongs to the company itself

The separation of amounts occurs only internally

This structure depends on an internal control system (ledger) of the fintech to separate customers' balances, which means that the individualization does not exist at the banking level, only at the system level.

In other words, although the customer has an “individual” balance within the platform, that amount is not linked to its own bank account.

Why does the mechanism exist

The pooled account model emerged as a way to simplify the operations of fintechs and companies that needed to move funds for multiple users.

Among the main reasons for its adoption are:

Reduced operational complexity

Less dependence on traditional banking infrastructure

Faster implementation of financial products

At a time when the market was still taking shape, this model allowed various companies to launch financial solutions with greater agility.

However, this simplification brought with it an important limitation: the lack of individualization in the financial system.

Is a pooled account illegal?

The omnibus account is not, by definition, illegal. However, the central point is not the model itself, but the way it is used.

With regulatory developments in Brazil, especially with increased oversight of payment institutions, a higher level of the following has come to be required:

Identification of the ultimate owner of the funds

Traceability of transactions

Operational transparency

Models that do not offer this clear individualization may be considered inadequate from a regulatory standpoint, especially in scenarios involving fraud risk, money laundering, or difficulty in judicial blocking.

In practice, this means that the omnibus account model has been increasingly pressured, not necessarily prohibited, but progressively replaced by more transparent structures.

The risks associated with the pooled account

The absence of individualization has significant implications for financial operations.

Court-ordered freezes

Since the funds are concentrated in a single account, any court-ordered freezes may affect the total balance, regardless of the source of the funds.

This kind of scenario creates a systemic risk: a single legal action can affect all users of the platform, even those who have no connection to the case.

Risk of money laundering

The lack of granular identification makes it difficult to track financial transactions.

For financial institutions and fintechs, this is not just an operational risk; it is also a regulatory risk that can lead to sanctions and operating restrictions.

Lack of transparency

Without proper segregation, it becomes harder to identify ownership of the funds, which can compromise audits and internal controls.

👉 To better understand how these risks affect companies in practice, also see: Can a pooled account freeze your operations? Understand the real risks

How does it work in practice

In day-to-day operations, the pooled account works based on a logical, not banking, separation.

The company maintains a central account at a financial institution while internally controlling users' balances.

This means that:

The bank sees only one account

The company manages multiple balances internally

Users have access to an “individual balance” within the platform

This difference between what exists in the banking system and what is controlled internally by the fintech is what creates the model’s main vulnerability.

What changes with the new rules

As Banco Central regulations evolve, there is a clear trend toward increasing demands for transparency and traceability.

This implies:

Greater need to identify ultimate beneficial owners

Reduction of centralized structures

Encouragement of individual accounts

This movement indicates a structural shift in the market: it is not just a regulatory adjustment, but a transition to more robust financial infrastructure models.

This scenario has led fintechs and companies to rethink their financial structures.

👉 See also: How fintechs are replacing the use of pooled accounts

Impacts for companies

Companies that use or depend on the pooled account model may face important challenges, such as:

Need to adapt to new regulatory requirements

Review of internal processes

Investment in technological infrastructure

In addition, the continued use of this model may limit the scalability of the operation in the long term.

Best practices for risk mitigation

Given this scenario, some practices can help reduce the risks associated with pooled accounts:

adoption of more robust user identification mechanisms

improvement of internal controls

increased transparency in operations

evaluation of alternative models

What is replacing the pooled account

As the market evolves, the main alternative to the pooled account model becomes the creation of individualized accounts, with greater transparency and traceability.

This type of structure requires a technological infrastructure capable of creating and managing accounts at scale, with balance control, transaction management, and integration with the financial system.

👉 Learn more: What are the alternatives to a pooled account (and how to choose the best structure)

👉 And also:How the infrastructure behind digital accounts works

It is at this point that Banking as a Service (BaaS) solutions allow companies to operate with individual accounts, while maintaining operational efficiency and regulatory compliance.

Final considerations

The omnibus account played an important role in the development of the digital financial ecosystem, especially at a time of lower regulatory and technological maturity.

However, with the evolution of the market and regulatory requirements, this model has been progressively replaced by more transparent and secure structures.

Companies operating in this sector need to keep up with this transformation and continuously assess the adequacy of their operations.

Modernize your financial infrastructure

If your company operates or plans to operate financial services, understanding the role of the pooled account is just the first step.

The next is to structure an operation that is secure, scalable, and aligned with regulation

Azify offers a complete Banking as a Service infrastructure for companies that want to build financial products with individual accounts, APIs, and integrated compliance.

Talk to a specialist and see how to evolve your operation beyond the pooled account.