With the growth of e-commerce and fintechs, customers around the world now expect to pay and receive in their local currency, in a simple and transparent way. In this scenario, multi-currency integration has ceased to be just a technological differential and has become a strategic necessity for companies that wish to compete globally.

After all, how to enable customers in Europe to pay in Euro, consumers in Latin America to use real or peso, and investors in the United States to transact in dollar, all within the same platform and with regulatory security? This is exactly what multi-currency integration provides.

In this article, you will understand how this model works, what benefits it generates, the main challenges, and how Azify can be your partner in the internationalization journey.

What is multi-currency integration and why is it important?

Multicurrency integration is the ability of a company to process payments and transactions in different currencies natively, offering customers the opportunity to buy, invest, or move resources in their own monetary language.

In the globalized world, this integration:

Reduces trade barriers: eliminates friction in currency conversion.

Improves customer experience: each user pays as they are accustomed to.

Increases competitiveness: opens doors to international markets without the need for multiple intermediaries.

A clear example is in transnational e-commerce: a virtual store that sells from Brazil to Europe and can receive directly in euros, without requiring the customer to calculate the conversion to reais or depend on international cards.

Informational content. Does not constitute an offer of securities, foreign exchange or payment services. Past performance does not guarantee future results. Azify operates directly or through duly authorized partners, as per the scope.

How does multi-currency integration work in practice?

In practice, multi-currency integration occurs through APIs, payment gateways, and modular solutions that connect the company to global financial networks.

APIs (Application Programming Interfaces): allow different systems to communicate with each other. A multi-currency API connects the company's platform to banks, acquirers, and global liquidity providers.

Payment gateways: act as the "bridge" that processes the transaction in different currencies, ensuring that the customer pays in their local currency and the company receives in a consolidated manner.

Modular solutions: allow the company to choose which currencies to offer, which markets to operate in, and how to configure embedded compliance for each region.

In practice, it's like your company has a universal cash register: the customer pays in Argentine pesos, you receive in Brazilian reais or dollars, and all of this with clear fees, correct regulatory records, and transparency.

What are the main benefits of multi-currency integration?

The multi-currency integration generates direct and strategic gains:

Global reach – Companies can operate in various countries without the need to create complex local structures.

Reduction of payment frictions – Eliminates manual steps and additional foreign exchange conversion costs.

Customer loyalty – Offering a local experience in a global business increases trust and recurring transactions.

Improvement in treasury management – Centralized reconciliation and automatic conversion allow for greater predictability in cash flow.

Regulatory compliance – With embedded compliance, the company operates smoothly in the face of local and international legislation.

Market studies show that offering local payment methods and pricing in local currency tends to increase the conversion rate. For example, Stripe reported an average increase of 7.4% in conversion by providing local methods, and a study from Continuum Commerce in the e-commerce sector reported a reduction of up to 50% in cart abandonment when enabling payments in local currency. These indicators reinforce the strategic value of multi-currency integration for international markets.

Which sectors benefit the most from multilateral currency integration?

Although all global businesses can benefit, some sectors have immediate gains:

Fintechs and digital banks: offer digital wallets, international cards, and global investment products.

E-commerce: increases sales by allowing checkout in the customer's currency.

Global marketplaces: connect buyers and sellers from different countries.

Online education and SaaS: allow billing in different currencies, reducing subscription barriers.

Travel and tourism companies: allow bookings and packages with local payments.

An example is Shopify, which expanded its customer base by offering multi-currency checkout in over 130 countries, increasing the adoption of merchants who export.

What are the main challenges of multi-currency integration?

Despite being attractive, multi-currency integration brings challenges that need to be managed:

Regulatory compliance – Each country has its own rules for currency exchange, taxation, and anti-money laundering.

Security – Adopting anti-fraud protocols, multi-factor authentication, and real-time monitoring is essential.

Currency management – Currency fluctuations impact margins. Therefore, robust solutions need to anticipate automatic conversions and treasury reporting.

Technological integration – Companies must integrate multiple financial systems without compromising the user experience.

In this context, the regulatory and technological expertise of Azify makes a difference, by offering a modular solution that is already designed to overcome these obstacles.

Success stories: who is already operating with multi-currency?

The multi-currency integration has ceased to be a unique advantage for large players and has become a competitive requirement in global markets. Companies that have adopted this model have not only expanded their international presence but have also gained more trust from customers by reducing payment barriers and offering personalized experiences in different regions.

Airbnb: allows hosts to receive in local currencies and travelers to pay in various global currencies, reducing friction and making the experience smoother.

Spotify: adjusts subscription prices according to the local currency, which has been crucial for expanding the user base in emerging markets and increasing accessibility to the service.

Nubank: offers an international card and direct exchange solutions integrated into the digital account, bringing the traditional banking experience closer to a global and more accessible model for its customers.

These examples show that companies investing in multi-currency integration achieve scale, trust, and greater adoption in different countries, consolidating a competitive positioning in the financial and digital landscape.

What are the global trends in multi-currency payments?

As international trade, fintechs, and digital platforms continue to grow, some trends are redefining the game for those who want to operate with multi-currency integration competitively. Here are recent data, digital currency initiatives, and the impact of stablecoins and CBDCs—all indicating that companies without this vision risk being left behind.

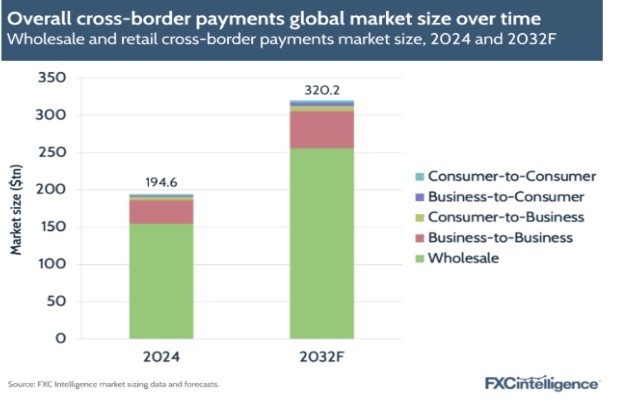

Growth in international transactions

Source: FXC Intelligence market sizing data and forecasts

The global cross-border payments market already handles colossal figures. According to data from FXC Intelligence, the volume surpassed US$ 190 trillion in 2024 and is expected to reach around US$ 320 trillion by 2032, with an estimated average annual growth rate between 6% and 7%. This pace shows how multi-currency integration is increasingly strategic to sustain global trade and financial flows.

In this context, stablecoins have been gaining prominence. In February 2025, the monthly transaction volume in these digital currencies exceeded US$ 700 billion, compared to approximately US$ 521 billion in the same period of 2024. Furthermore, the number of active monthly addresses has surpassed 30 million, signaling that usage is not limited to speculation but is consistently spreading across different regions and user profiles.

The advancement is even more evident when observing market capitalization. In September 2025, stablecoins surpassed the US$ 300 billion mark for the first time—a jump of more than US$ 100 billion in just one year. This significant growth consolidates USDT and USDC as the main liquidity benchmarks in the ecosystem, demonstrating that the digitalization of money already directly impacts the future of international payments.

The advancement of stablecoins as part of a multi-currency strategy

Stablecoins have been gaining prominence as a key piece in multi-currency integration. Among them, USDT and USDC broadly dominate the market, together accounting for about 86.5% of the total value issued globally.

The trajectory of USDC deserves attention: in 2025, its annual growth rate reached approximately 40.9%, according to a report from PANews Lab. If this pace is maintained, analysts project that the currency could surpass USDT in market volume by 2030, changing the leadership in this strategic segment.

In addition to handling large volumes in crypto assets, stablecoins have been increasingly used in international remittances, micro-payment settlements, and even as a hedge alternative in economies with high inflation. This growing usage reinforces that it is not just about speculation but a real tool for efficiency, accessibility, and stability in the global financial ecosystem.

Central Bank Digital Currency (CBDC) and digital euro initiatives

The European Union, through the European Central Bank (ECB), is advancing in the development of the digital euro, a central bank digital currency (CBDC). The goal is to provide a public and secure alternative to the electronic money already in use today, strengthening European sovereignty in payment systems and responding to the advance of private stablecoins, such as USDT and USDC.

Currently, pilot projects are already underway. European fintechs are participating in tests involving payment infrastructure, issuance of local stable tokens, and regulatory adaptation. All of this occurs under the MiCA (Markets in Crypto-Assets) regime, which establishes clear guidelines for the crypto asset ecosystem in the region.

This movement positions Europe as a key player in the global debate on sovereign digital currencies, demonstrating that multi-currency integration is directly linked to the regulatory and technological transformations of the international financial system.

All these trends together point to some important implications for those considering operating globally:

Regulatory pressure will increase: stablecoins and CBDCs are on regulators' radars. Those who already have compliance structures in place will have an advantage.

User experience expectations are rising: customers will prefer platforms that allow payments in their local currency, with transparency in conversion fees, avoiding unpleasant surprises.

More sophisticated technological solutions will be in demand: multi-currency requires robust API integration, payment gateways that support multiple currencies, currency exchange automation, monitoring, etc.

Informational content. It does not constitute an offer of securities, currency exchange, or payment services. Past performance does not guarantee future results. Azify acts directly or through duly authorized partners, as per the scope.

How do these trends strengthen competitive advantage?

The growth trends of international transactions, the expansion of stablecoins, and the advancement of central bank digital currencies (CBDCs) show that global companies need solutions that combine flexibility, security, and compliance from the outset.

Azify offers multi-currency integration from the conception, working with partners who operate under global regulatory regimes and keeping pace with the growth of stablecoins and the development of CBDCs. This approach allows your company to accept payments in local currencies and regulated stablecoins while remaining aligned with frameworks such as MiCA and national regulations, reducing regulatory risks and increasing operational reliability.

Moreover, global clients value predictability: transparent exchange rates, clear settlement, and built-in compliance make any operation safer and more reliable. By positioning its services this way, Azify ensures that your company is ready to compete internationally with secure and scalable innovation.

The multi-currency integration is more than just a financial solution: it is a global competitiveness strategy. Companies that adopt this approach are able to scale operations, retain customers, and gain agility in an increasingly connected market.

With modular solutions and embedded compliance, Azify is the ideal partner for fintechs, e-commerce, and marketplaces that wish to expand without borders. Talk to our team to understand the applicable scope for your business.