Stablecoins have moved beyond a concept restricted to the crypto market and have come to play an increasingly relevant role in global financial infrastructure.

Today, companies use stablecoins to make international payments, reduce operating costs, and increase financial predictability, especially in cross-border operations.

If you still associate stablecoins only with trading or crypto assets, it's worth updating that view.

In this complete guide, you'll understand:

What stablecoins are

How they work in practice

What the main types are

Risks and regulation

How companies are using stablecoins in cross-border payments

What are stablecoins?

Stablecoins are digital assets designed to maintain a stable value in relation to a fiat currency, such as the dollar or euro.

In practice, this means that a stablecoin like USDT or USDC seeks to maintain parity with the dollar (1:1).

Unlike traditional cryptocurrencies, such as Bitcoin, which can be highly volatile, stablecoins arise precisely to solve this problem: allowing the use of digital assets without significant exposure to price fluctuations.

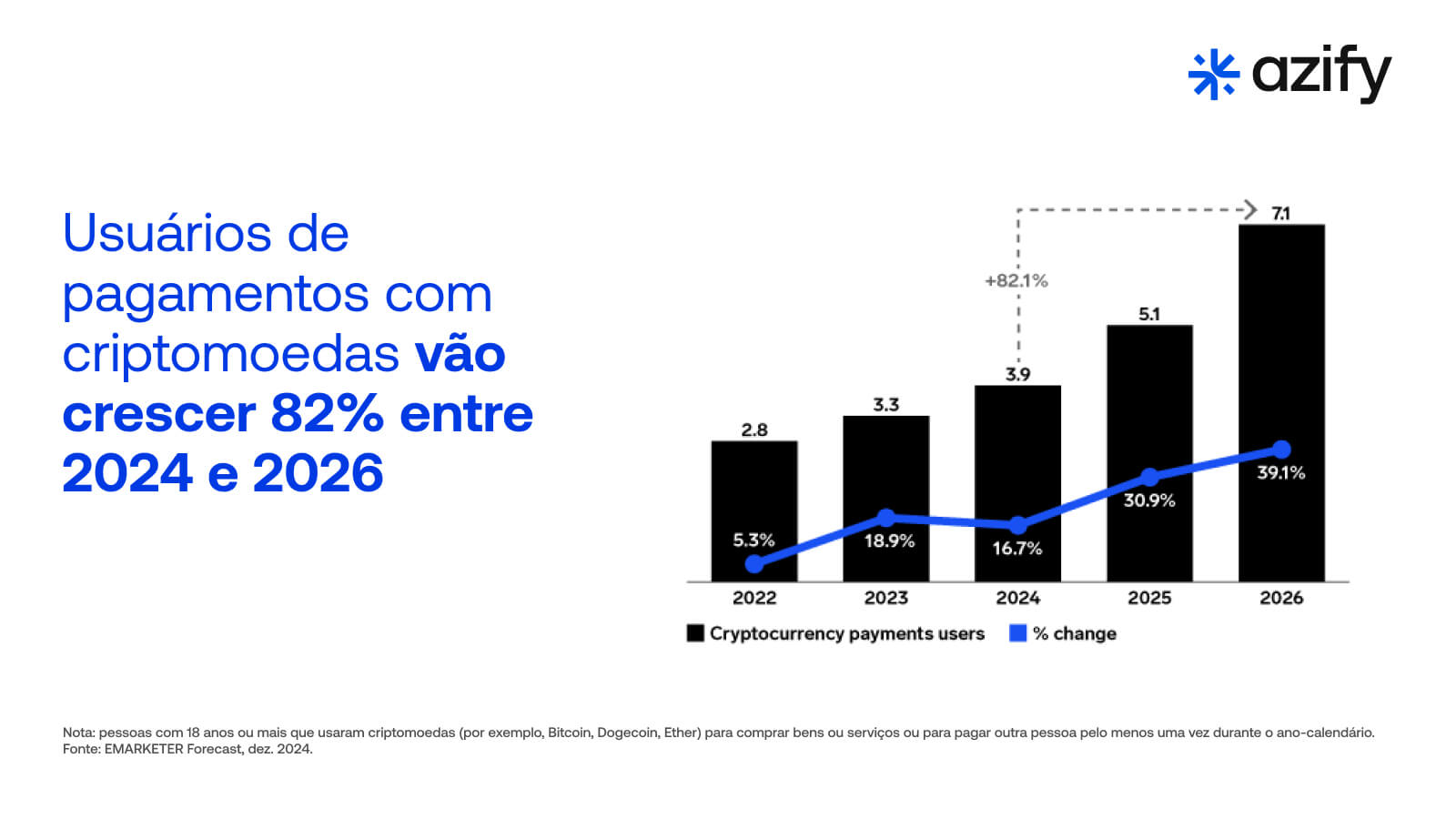

Why have stablecoins gained so much relevance

Stablecoins have grown rapidly because they solve a real problem: transferring value globally in a fast, programmable way with less friction.

As shown in the original article itself, they have become a central part of the crypto ecosystem and are already widely used for:

Trading and liquidity on exchanges

Protection against inflation in some countries

International payments

Institutional operations

But the most relevant point, especially for companies, is another one:

👉 stablecoins are becoming a new infrastructure for international payments.

If you want to better understand this context, it's worth reading our guide oncross-border payments and how they work for businesses.

How stablecoins try to maintain parity

There are some mechanisms for bringing the stablecoin's market value closer to the reference asset:

Fiat-backed (fiat)

The issuer holds reserves in cash, short-term government bonds, and other highly liquid assets, theoretically equivalent to the number of tokens issued. USDT and USDC are the classic examples.

Crypto-backed assets

Protocols like DAI use collateral in BTC, ETH, or other tokens. They generally require “overcollateralization”: to issue 100 in stablecoins, you lock up 150 or 200 in crypto, for example, to absorb volatility. Commodity-backed

Some are tied to gold or other physical assets, keeping the equivalent in custodial reserves.

Algorithmic mechanism

An algorithm adjusts supply and demand (burning and issuing) to try to keep the price stable as long as the incentives work. This model lost credibility after famous collapses such as TerraUSD.

In practice, the market today is dominated by fiat-backed stablecoins, which is the simplest model to understand and the one most favored by regulators and institutions.

What do companies use stablecoins for in practice?

Although use in trading is the best known, the most relevant growth is in corporate use. Companies use stablecoins for:

International Payments/International Remittances/Cross-Border

Faster global transfers with fewer intermediaries.

This is one of the main use cases and is directly related to the topic of international payments for businesses.

Global liquidity management

Companies operating in multiple countries use stablecoins to move funds more efficiently.

Cost reduction

By reducing intermediaries and optimizing the settlement infrastructure, it is possible to lower operating costs.

24/7 operations

Unlike the traditional banking system, stablecoin transactions can occur at any time.

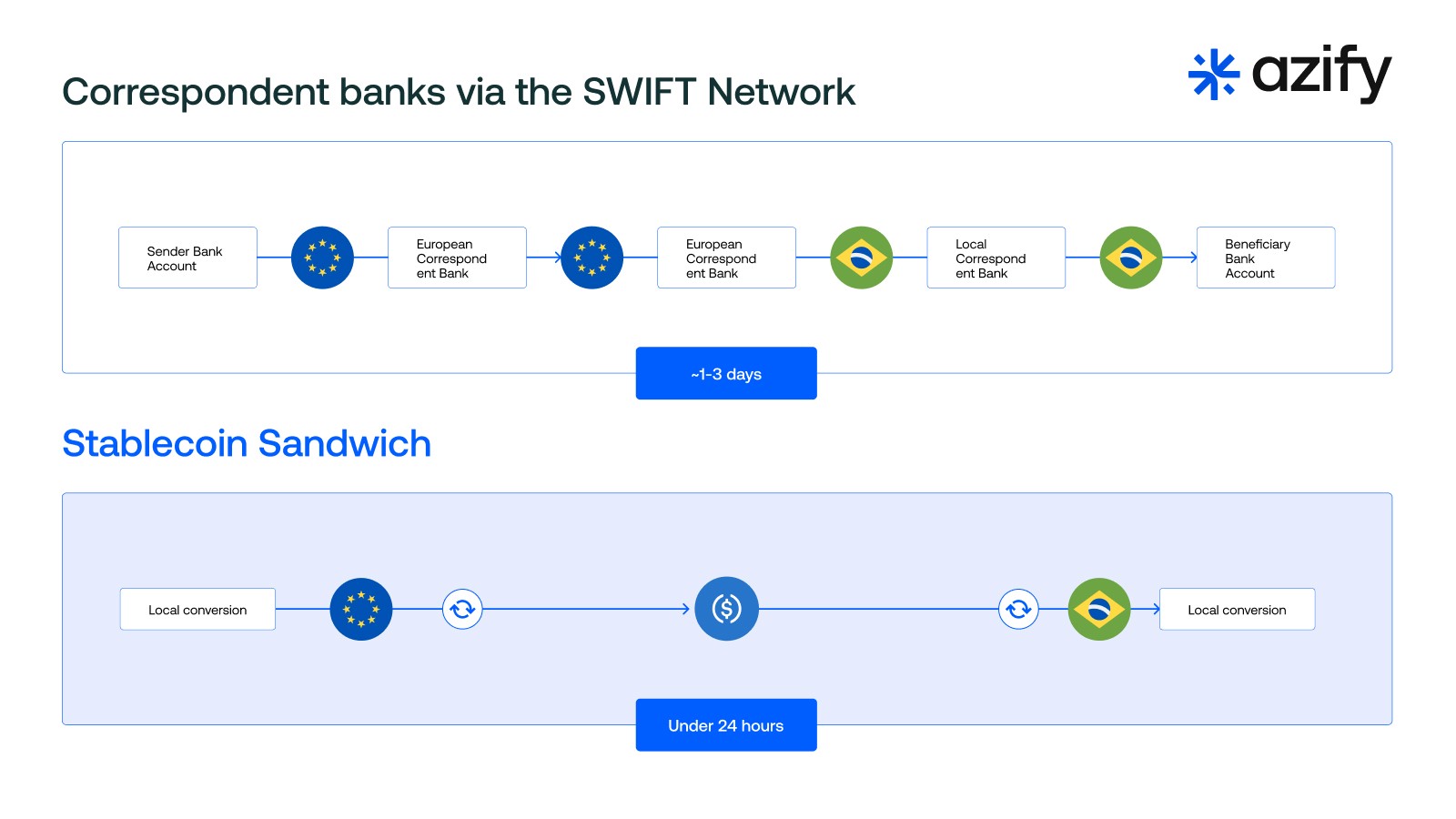

How are stablecoins used in international payments

Stablecoins do not replace the financial system; they act as a settlement layer.

In practice, the flow works like this:

Conversion of local currency into stablecoin (on-ramp)

Digital transfer via blockchain

Conversion to local currency at the destination (off-ramp)

This model reduces settlement time, the number of intermediaries, and operational costs.

If you'd like to better understand this flow, also see:

👉 How USDT-to-real conversion works

👉 And how much an international transfer for companies costs

Overview of the main dollar stablecoins

Here come the stars of the game. Let's go through the ones you explicitly requested: USDT, USDC, USD1, and PYUSD.

USDT (Tether)

Largest stablecoin in the world by market value, with tens of billions of dollars in circulation.

Issued by Tether, linked to the Bitfinex exchange.

Reserves today are largely short-term U.S. Treasury securities, to the point that Tether has become one of the largest global buyers of Treasuries and influences their yields.

On one hand, it is omnipresent on exchanges around the world and has absurd liquidity. On the other hand, it has faced regulatory scrutiny, fines, and periods of less transparency about reserves, which leads many people to prefer diversifying their risk.

USDC (USD Coin)

Issued by Circle in partnership with Coinbase, under a model of 100% reserves in cash and high-quality securities, with regular audits and public reports.

Widely used by companies and DeFi protocols that value transparency and integration with the traditional banking system.

USDC tends to be perceived as “more regulated” and aligned with the financial mainstream, making it a favorite among institutions, even having temporarily lost its peg during events such as the Silicon Valley Bank crisis.

USD1 (World Liberty Financial USD)

Dollar stablecoin launched by World Liberty Financial, a project linked to the Trump family, positioned as “institutional-ready.”

Reserves held by the custodian BitGo, with a significant portion in short-term Treasuries, aligned with the USDT and USDC models.

The company plans to use USD1 as a basis for tokenizing real-world assets (RWA) such as oil, gas, and others, starting in 2026.

USD1 is a good example of the new wave: the stablecoin is already connected with RWA products, aiming for institutional and sovereign use. The downside is a higher level of politicization around the issuer.

PYUSD (PayPal USD)

Dollar stablecoin from PayPal, issued by Paxos, with reserves in bank deposits and short-term Treasuries, redeemable 1:1 in dollars.

Integrated into the PayPal and Venmo ecosystem, with hundreds of millions of users, which positions it well for payments and digital commerce.

In practice, PYUSD aims to be the “retail” stablecoin, focused on payments and integration with merchants, rather than in hardcore trading use.

Euro stablecoins: EURC and EURCV in the spotlight

While the dollar dominates the global stablecoin market, the euro game has started to heat up with the MiCA regulation in the European Union.

EURC (Circle)

A fully euro-backed stablecoin, issued by Circle, the same company behind USDC.

Operates on multiple networks, such as Avalanche, Base, Ethereum, Solana and Stellar.

It is MiCA compliant and works on a full-reserve model, with 1:1 redemption in euros.

EURC positions itself as the euro stablecoin most aligned with European regulation, and has been driving much of the growth of the euro stablecoin market after MiCA.

EURCV (EUR CoinVertible)

Issued by Société Générale–Forge, the crypto arm of Société Générale. S

Created in 2023, it was restructured in 2024 to become an “open” stablecoin, MiCA-compliant and transferable without restrictive whitelists.

Initially focused on institutional use, such as a bridge between traditional markets and DeFi.

With MiCA in force, EURC and EURCV are two of the main forces in the euro stablecoin market, which doubled in size over the last year and is already moving hundreds of millions of dollars in market value.

Main risks of stablecoins

Despite the name “stable,” the risk does not disappear; it just changes form. The main ones:

Backing and trust risk

If the issuer does not have sufficient reserves or if the market loses confidence, the price can break parity. Notable cases have shown that, in times of stress, even large stablecoins can trade at a temporary discount relative to $1.

Regulatory risk

The ECB, for example, has already warned that large stablecoins can pressure the Treasury market if there is a run on redemptions.

In Europe, MiCA has brought a specific framework for e-money tokens and large-scale stablecoins.

In the U.S., the environment swings between greater openness and tighter oversight, with bills like the Genius Act seeking to regulate issuers.

The bottom line is: the regulatory landscape is evolving. What is permitted today may change, bringing new requirements for capital, transparency, and issuance limits.

Custody and technology risk

Losing the seed phrase or private keys means losing access to the balance.

Platforms can suffer hacks, freezes, or bankruptcy, as has happened in the crypto world more than once.

Concentration risk

The market is extremely concentrated among a few issuers. Recent reports indicate that Tether and Circle account for something close to 90% of the volume of stablecoins in circulation, which makes any problem at those issuers a systemic risk.

Regulation, CBDCs, and the future of stablecoins

Stablecoins also shook central banks' pride. Suddenly, private companies were issuing “almost money” on a global scale.

Responses to this:

MiCA in the European Union sets specific rules for stablecoin issuers, requiring additional capital, governance, and transparency, especially for significant tokens.

CBDC projects (central bank digital currencies) such as the digital euro and the Digital Real/Brazil’s Central Bank seek to offer a public, regulated, and programmable version of official currency.

In several scenarios, the trend is not “either stablecoin or CBDC,” but coexistence: stablecoins as a market and innovation layer, CBDCs as base infrastructure. In parallel, private banks are beginning to launch their own stablecoins, such as qivalis in Europe or Société Générale's initiatives with EURCV.

Conclusion: stablecoin is a tool, not a miracle

Stablecoins are a central piece of the new digital financial infrastructure. They make it possible to bring traditional money onto the blockchain with price stability, opening space for near-instant global payments, DeFi, asset tokenization, and innovation at scale.

But that does not mean they are risk-free. The risk moves away from “the price swings every day” and into other places: backing quality, governance, changing regulations, and market concentration in a few giant issuers.

When you look at USDT, USDC, USD1, PYUSD, EURC and EURCV, you are looking at a kind of real-time global laboratory: traditional banks, big techs, crypto giants, and even politicians competing to see who will be the trust layer of digital money.

If the idea is to use stablecoins responsibly, think of them as high-impact tools, not as “magic dollar savings.” Study the issuer, understand the reserves model, follow regulations, and, above all, do not put any amount into a digital asset that you could not tolerate seeing locked in case of a problem.

Money is still yours, but the architecture that moves it is changing quickly. Stablecoins are precisely the most visible interface of this transition between the old financial system and the new world of digital assets.

Do you want to use stablecoins in practice?

If your company makes international payments or operates globally, it is worth understanding how stablecoins can improve your operations.

Azify offers a complete infrastructure for international payments using digital assets in a transparent, secure, and integrated way.

Talk to an Azify specialist and see how to apply stablecoins in your operations.