In the current scenario, launching financial products quickly and securely can be a challenge for companies that are not banks. Banking as a Service (BaaS) emerges as a strategic solution, allowing companies to offer services such as digital accounts, payments, and cards, always through authorized partners and within the regulatory scope. In this article, you will understand how BaaS works, when it makes sense to adopt it, and what regulatory and operational care is essential to reduce risks.

What is Banking as a Service (BaaS) and why does it matter?

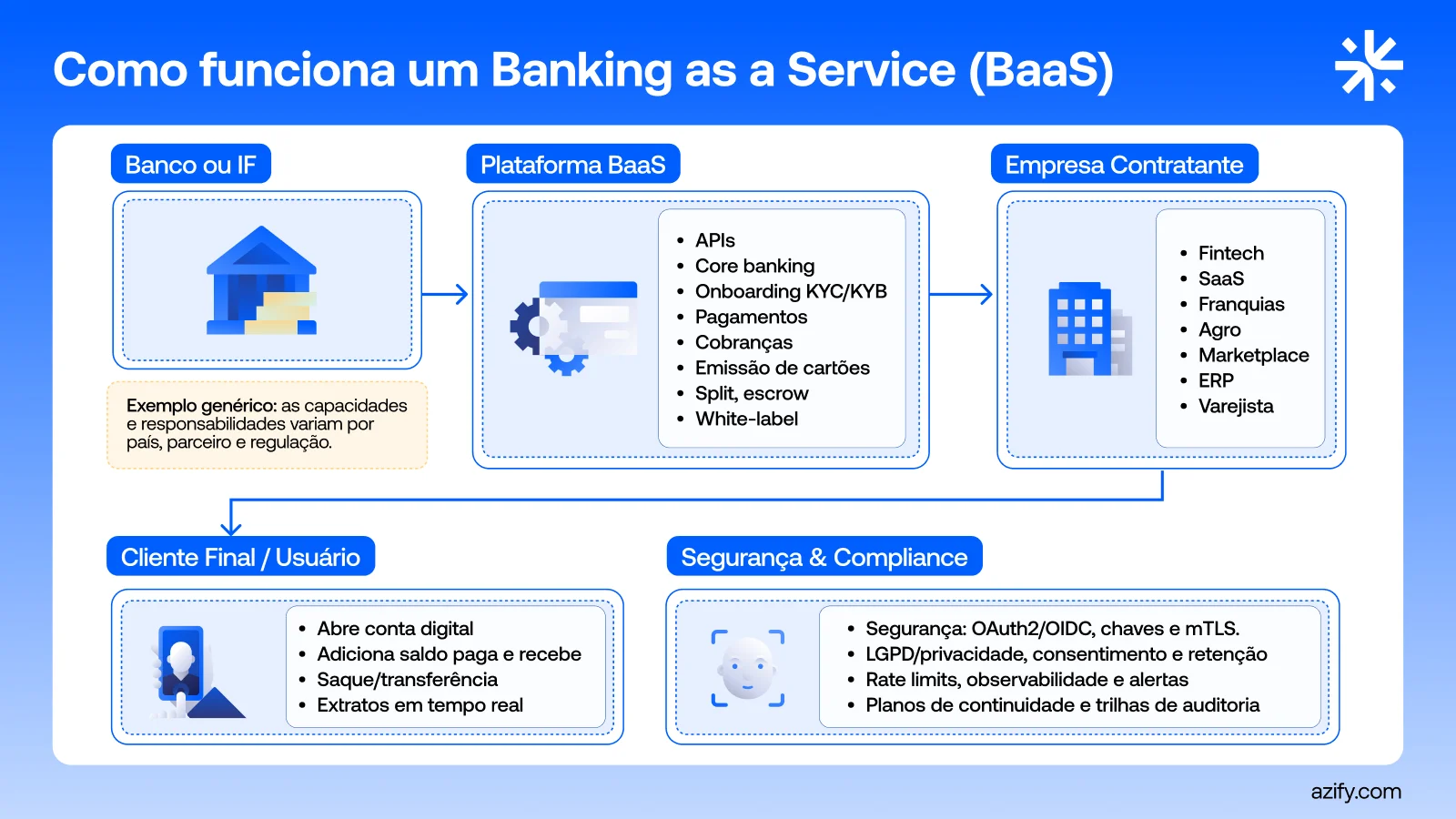

The Banking as a Service (BaaS) is a solution that allows companies to offer financial products and services without needing to build the entire infrastructure of a traditional bank. In other words, it’s like having a ready-made road for your car, without needing to lay the asphalt, allowing the operation to be fast, scalable, and secure.

With BaaS, companies from different sectors — such as fintechs, startups, marketplaces, and digital retailers — can provide complete financial services to their clients, including:

Digital accounts: opening, maintenance, and movement of funds, with the company’s own interface.

Payments and transfers: instant and programmable operations, integrated into the user experience.

Credit or debit cards: issuance of physical or virtual cards, customized and with control from the end customer.

Credit and loan solutions: from lines of credit for clients to product financing, via regulated partners.

This entire ecosystem operates through authorized partners, ensuring that each operation is compliant with Bacen, CVM, CONAR, Law 14.478/2022, and other applicable regulations. It is essential to highlight that the company adopting BaaS does not act as a financial institution or offers currency exchange or payment services directly, but rather exposes its clients to products and solutions from regulated partners, maintaining legal, operational, and regulatory security.

Furthermore, BaaS allows companies to monitor all transactions, reports, and compliance indicators in an integrated manner, providing greater transparency, auditability, and control over the customer’s financial experience.

Important: informational content. Does not constitute an offer of securities, currency exchange, or payment services. Past performance does not guarantee future results. Azify acts directly or through duly authorized partners, as per the scope. Assess risks, accounting, and tax impacts with your advisors.

How does BaaS differ from traditional banking models?

The main difference lies in the speed and flexibility. While creating a bank from scratch requires years of investment and complex regulatory processes, BaaS allows:

To launch financial products quickly

To integrate services via standardized APIs

To customize the customer experience without compromising security

Furthermore, BaaS provides full observability of operations, allowing transaction monitoring, auditing, and compliance reporting.

Safe opening checklist in BaaS

Approved and documented APIs

Defined SLA with partners

KYC, PLD, and combating terrorism financing (CTF)

Audit and compliance reports

Clear limits on financial exposure

What is the size of the global Banking as a Service market and what trends does it reveal?

The growth of Banking as a Service (BaaS) is not just a fleeting trend, but a consolidated global movement. According to Grand View Research, in the report Global Banking as a Service Market, 2018-2030 the global BaaS market generated approximately USD 22.4 billion in 2022 and is projected to reach USD 74.5 billion by 2030, with a compound annual growth rate (CAGR) of 16.2% between 2023 and 2030.

This rapid advancement is directly linked to the demand for digital financial platforms, which allow companies from different sectors to offer banking services in a modular way, without needing to build all the infrastructure from scratch. In 2022, the platforms segment was the most profitable, accounting for more than half of the global revenue, and is also projected to be the fastest-growing for the coming years.

When we look at the geographical distribution, North America led in 2022, accounting for approximately 33.7% of global revenue, driven mainly by the market in the United States, which is expected to continue growing rapidly until 2030. In the Asia-Pacific region, countries like China, India, and Japan are also increasing investments, reflecting the accelerated digitalization of their financial systems.

These numbers reinforce that BaaS has ceased to be just a bet for the future and has already established itself as a strategic solution in the present. For companies looking to scale their businesses, market data indicates that the adoption of Banking as a Service models may not only become a competitive differentiator but a necessity to keep up with the transformation of the global financial sector.

What are the main benefits of Banking as a Service?

Banking as a Service (BaaS) is not just a practical alternative to the traditional banking model — it transforms the way companies launch and manage financial products, bringing benefits that go beyond operational agility. Among the main benefits are:

1. Agility in product launch – With BaaS, your company does not need to invest years in its own financial infrastructure. It is possible to quickly launch digital accounts, credit or debit cards, payment lines, and even credit solutions, supported by partners approved by Bacen and in compliance with the Law 14.478/2022. This speed allows companies to test new products in the market, adjust functionalities, and respond quickly to customer needs without compromising security or compliance.

2. Reduction of regulatory risks – By operating via BaaS, your company functions within a secure regulatory scope, minimizing exposure to legal issues related to Bacen, CVM, LGPD, or regulatory agencies. As operations rely on approved partners, it is possible to offer financial services without becoming a financial institution, maintaining legal security and ensuring that all KYC, AML/CFT, and audit processes comply with existing regulations.

3. Scalability and operational flexibility – BaaS solutions are based on robust APIs, which allow for scalable financial products in a modular manner. Companies can expand operations, integrate new services, or meet demand spikes without needing to invest in their own servers or large technical teams. For fintechs, marketplaces, and digital platforms, this means rapid growth without increasing operational risks.

4. Personalization and customer experience – Even without operating as a bank, your company can offer fully customized financial products, with its own interface, branding, and user experience flow controlled internally. This includes personalization of limits, notifications, dashboards, and reports for end customers. By combining user experience with regulatory security, BaaS allows for the creation of solutions that meet both compliance needs and customer expectations for convenience and usability.

What regulatory and compliance measures are essential?

The BaaS involves critical compliance aspects that must be carefully observed:

KYC (Know Your Customer) and AML/CFT: ensuring customer identification and money laundering prevention

Compliance with Law 14.478/2022: regulates digital asset offerings and financial services in Brazil

LGPD: protection of personal data of customers

Dependence on regulated partners: all financial operations must be conducted through authorized institutions

Audit checklist: monitor SLAs, reports, and risk indicators

Key compliance points in BaaS

Documentation of partner approvals

Continuous monitoring of transactions

Periodic reports for regulatory agencies

Constant regulatory updates

How to evaluate BaaS providers: technical and regulatory criteria

Choosing a reliable Banking as a Service (BaaS) provider goes far beyond comparing prices or basic features. It is necessary to conduct a detailed assessment that combines technical, operational, and regulatory aspects, ensuring that your company operates safely and within the law.

Regulatory authorization – The first step is to confirm that the provider is properly registered with the competent authorities, such as Bacen, CVM or other specific regulators. This verification ensures that the financial services offered — such as digital accounts, transfers, or card issuance — are legally supported and that the company will not be exposed to risks of irregular operation.

API infrastructure and operational reliability – The API integration is the heart of BaaS. It is essential to evaluate:

Complete, clear, and up-to-date technical documentation;

SLA (Service Level Agreement) defined, with metrics for availability, response time, and support;

Continuous monitoring of the infrastructure, including failure alerts and scalability capacity.

These points reduce the risk of service interruptions and ensure a reliable experience for your customers.

Data security and protection – The provider must fully comply with the LGPD, implementing robust cybersecurity, practices such as data encryption in transit and at rest, multi-factor authentication, and intrusion prevention protocols. Security is not just technical: internal access policies and periodic audits are also essential to protect sensitive information.

Governance and auditing – A good provider maintains regular reports and compliance reviews, allowing your company to track all transactions, incidents, and operational adjustments. Governance includes:

External and internal audits;

Documentation of compliance policies;

Periodic risk and performance reports, which may be required by regulators.

Scope of services and legal limits – Finally, it is crucial to confirm that the provider offers exactly the services you need, without exceeding regulatory limits. This includes:

Checking that the financial products offered are within the allowed scope;

Ensuring that the integrations do not create direct exposure to foreign exchange or payment services without authorization;

Assessing whether there is sufficient flexibility to grow or adapt products, always respecting the applicable regulations.

BaaS Provider Evaluation Checklist

Registration and regulatory authorization

Documentation and SLA for APIs

Data security and LGPD compliance

Governance, auditing, and periodic reports

Adherent service scope and clear limits

By following these criteria, your company can select trustworthy partners, reduce regulatory and operational risks, and build secure and scalable financial products.

BaaS and fintechs: accelerating products safely

For fintechs, BaaS is a strategic tool. It allows startups to launch financial solutions without needing to become a bank, reducing costs and regulatory complexity.

Example: A fintech can launch a digital account for instant payments using APIs from an authorized BaaS partner, maintaining control of the interface and user experience, but not operating as a financial institution.

BaaS APIs: features and considerations for integration

The Banking as a Service (BaaS) APIs are the core that connects the financial infrastructure of the provider to your company's applications. They allow for the automation of processes and offer personalized services to clients while maintaining operational and regulatory control. Among the main features are:

Opening digital accounts: creating accounts for clients quickly and automatically, including data validation and integration with KYC and AML/CFT systems.

Financial transactions: transfers, payments, and deposits can be made in real-time, with complete traceability of transactions.

Issuance of cards: generating physical or virtual cards, managing limits, blocks, and integrations with recognized brands, all within regulatory standards.

Detailed transaction reports: extraction of financial data and periodic reports for auditing, compliance, and risk monitoring.

To ensure security and compliance, it is essential to observe some precautions in integrating the APIs:

Validate financial exposure limits: define operational ceilings and monitor transactions to avoid liquidity risks or excessive exposure.

Monitor logs and security events: track errors, fraud attempts, or suspicious behavior in real-time, with automatic alerts when necessary.

Ensure compatibility with audits and regulatory reports: maintain complete, auditable records aligned with Bacen, CVM, and internal compliance requirements.

Continuous updates: keep up with regulatory changes and provider improvements to ensure that integration remains secure and efficient.

Tip: before activating new APIs, conduct a homologation test in a secure environment to identify possible failures or inconsistencies in the integration, avoiding impacts on customer experience and regulatory compliance.

Best practices in BaaS APIs

Technical homologation before launch

Continuous monitoring of errors and performance

Automatic alerts for suspicious transactions

Periodic updates according to regulations

What is Liquidity as a Service (LaaS) and how does it connect to BaaS?

The Liquidity as a Service (LaaS) is a strategic solution that provides immediate liquidity for financial transactions, ensuring that companies and platforms can meet payments and movements quickly and efficiently. This service is particularly relevant for crypto asset exchanges, OTC desks, fintechs, and trading platforms, where the speed and availability of financial resources are critical for secure and continuous operation.

LaaS allows your company to:

Facilitate instant payments, eliminating delays in transfers between accounts or platforms

Reduce liquidity bottlenecks, ensuring that there are always funds available for client or partner transactions

Integrate with BaaS solutions, creating a complete and smooth financial experience by combining digital account management with the liquidity necessary for complex operations

For example, a crypto asset exchange can use LaaS to maintain constant liquidity in trades, while BaaS manages digital accounts, card issuance, and client fiat movements, allowing the entire operation to function in an integrated, secure manner and within the regulatory scope.

Moreover, LaaS offers real-time liquidity monitoring, financial exposure reports, and integration with audits, helping your company mitigate operational and regulatory risks, maintaining compliance with Bacen, CVM, and applicable regulations.

LaaS for exchanges and OTC desks: possibilities and limits

For OTC desks and exchanges, the LaaS offers:

Agility in liquidity

Ability to meet peaks in demand

Operations within regulatory limits

Important limits:

Depends on authorized partners

Maximum exposure defined by contract

Compliance with KYC, AML/CFT, and Bacen

Blockchain and BaaS/LaaS: fundamentals and applications

The blockchain is the technology that ensures secure, transparent, and immutable recording of transactions, functioning as a shared digital ledger among multiple parties. In Banking as a Service (BaaS) and Liquidity as a Service (LaaS) solutions, blockchain offers strategic benefits that go beyond security:

Complete traceability of transactions: each movement is recorded in sequential blocks, allowing for detailed auditing and quick detection of inconsistencies or suspicious activities.

Process automation with smart contracts: smart contracts can automatically execute predefined rules, reducing operational errors, speeding up payments, and ensuring that regulatory conditions are met before executing any operation.

Reduction of intermediaries and costs: as the technology enables direct and verifiable transactions between authorized parties, it is possible to lessen the reliance on traditional intermediaries, optimizing financial and operational resources.

Compliance applied to blockchain

The use of blockchain in BaaS and LaaS also strengthens regulatory compliance, offering mechanisms that support audits and data protection:

Auditable smart contracts: each execution is recorded immutably, facilitating review by internal or external auditors and ensuring transparency before regulatory bodies.

Formal operation records: all movements are available for consultation, creating a reliable history for reports required by Bacen, CVM, or other competent authorities.

Protection of sensitive data via encryption: confidential information of clients or transactions is encrypted, reinforcing adherence to LGPD and mitigating risks of leaks or unauthorized access.

Example: a fintech that offers digital accounts via BaaS may use blockchain to record each transaction, ensuring traceability, automatic execution of compliance rules, and security of client data, without compromising the user experience.

What are the risks and how to mitigate them?

Even with regulated partners, there are risks:

Technology integration risk: failures in APIs or SLAs

Regulatory risk: changes in legislation or interpretation of rules

Operational risk: poorly structured internal processes

Liquidity risk: reliance on partners in LaaS

Mitigation:

Constant monitoring of operations

Regular auditing of partners

Updating internal compliance policies

Continuous training of the team

Important: informational content. It does not constitute an offer of securities, currency exchange, or payment services. Past profitability does not guarantee future results. Azify operates directly or through duly authorized partners, as per the scope. Evaluate risks, accounting, and tax impacts with your advisors.

What are the practical cases of BaaS application?

The Banking as a Service is not just a theoretical concept: several companies already use this solution to accelerate financial products, optimize operations, and ensure regulatory compliance. Below, we present real examples of how startups, fintechs, and exchanges practically and securely apply BaaS and LaaS.

1. Payment Startup

A payment startup can launch digital accounts and cards using BaaS without needing to become a bank. The significant difference is that the company maintains its own interface and user experience, while all financial operations are conducted by an authorized partner, ensuring legal compliance. This model allows for quick launching of new products, testing functionalities, and scaling the service without large investments in financial infrastructure.

2. Credit Fintech

Fintechs focused on loans can integrate BaaS and LaaS APIs to offer instant credit. With BaaS, the management of accounts and fiduciary transactions is automated, while LaaS provides immediate liquidity for loans to be granted safely. This combination ensures operational agility, regulatory monitoring, and risk mitigation, allowing the fintech to focus on credit analysis and customer experience.

3. Crypto Asset Exchange

Exchanges and OTC desks can benefit from LaaS to ensure immediate liquidity in crypto asset transactions, while BaaS manages fiduciary movements, payments, and deposits. This model creates a hybrid structure, secure and scalable, in which the company can operate within clear regulatory limits, maintaining auditing, traceability, and compliance with the norms of Bacen, CVM, and LGPD.

Practical Benefits of BaaS and LaaS

Agility in launching financial products

Reduction of regulatory risks

Scalability without the need for proprietary infrastructure

Personalized user experience

Observability and continuous auditing

The Banking as a Service enables companies to launch financial products quickly, with regulatory safety and a personalized experience for clients. Meanwhile, Liquidity as a Service offers immediate liquidity, essential for complex operations, especially in fintechs, exchanges, and digital platforms, always within the limits and compliance required by the market. Talk to our team to understand the scope applicable to your business.